Understanding the cash flow statement and its implications for buyers (Part 3)

In the previous posts, you understood the role of the income statement and the balance sheet for buyers. Today I’ll continue exploring the final component of the financial statements: the cash flow statement. This document describes how much money flow in and out of the business over a period of time.

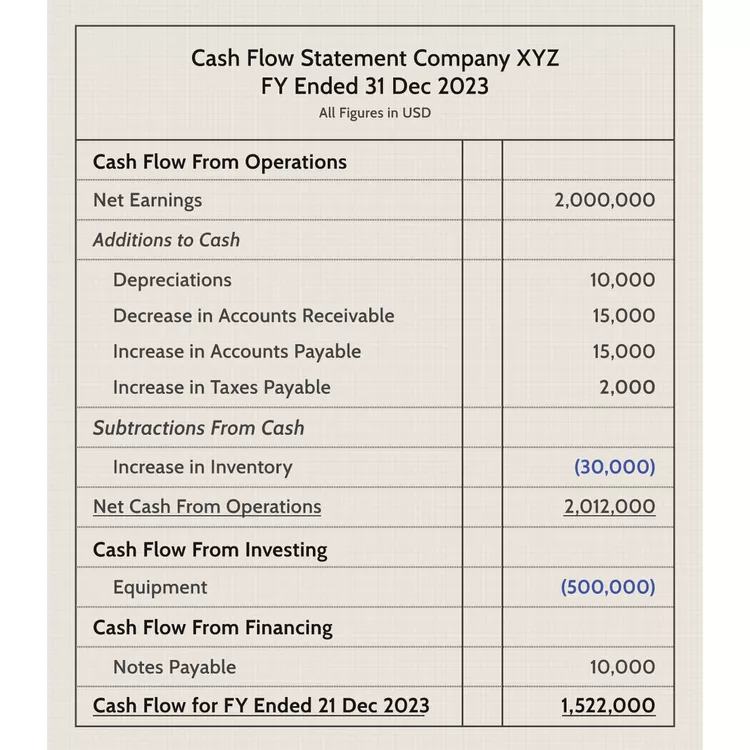

I’ve attached an example of a company’s cashflow statement in 2023. Normally, the income statement is structured into 3 sections: cash flow from operating activities, cash flow from investing activities and cash flow from financing activities.

Operating activities:

This section tells buyers how much cash a company cash a company has spent on or earned from its core business operations. When analysing cash flows, we need to categorize them into cash inflows and cash outflows. Cash inflow refers to money coming into the business while cash outflow is money going out of the business. As you can see in the example:

- Net Income: The net income is USD 2 million, which means the cash inflow is also USD 2 million.

- Depreciation: This expense is incorporated in both the balance sheet and the income statement. It increases the business’s cost on paper, but there is no actual cash outflow associated with it. This is why cash flow from operating activities takes depreciation into account to reflect the true amount of cash on hand.

- Decrease in Accounts Receivable: This reflects money flowing into the business through customer payments, amounting to USD 15,000.

- Increase in Accounts Payable: This refers to payments owed to suppliers or other parties that have not yet been paid. Therefore, the money remains in the business’s account, contributing USD 15,000 to the cash flow in the example above.

- Increase in Taxes Payable: This represents money owed to the government but not yet paid. As a result, it increases a company’s cash inflow.

- Increase in Inventory: This indicates a rise in inventory value, meaning the company spent money on raw materials or components to support production. Since this is a cash outflow, the amount USD 30,000 is shown in parentheses.

The net cash from operations = Net earning + Depreciations + Decrease in accounts receivable + Increase in accounts payable + Increase in taxes payable – Increase in inventory = USD 2,012,000.

Positive cash flow from operations implies that a company is operating efficiently and has the potential to grow in the future, while negative cash flow from operations indicates that a company may struggle to operate its core business activities.

Investing activities

This section describes cash used or received from investing activities. Like operating activities, it is categorized into cash outflows and cash inflows.

- Cash outflows typically include the purchase of property, investment securities, loans made to other entities, or acquisitions of other businesses.

- Cash inflows include proceeds from the sale of property, investment securities, or loan repayments received.

According to the example, the cash flow from investing includes only one expense: equipment purchase amounting to USD 500,000. This purchase reduces the company’s total cash, so the value USD 500,000 is placed in parentheses. Therefore, the net cash flow from investing is (USD 500,000).

When cash flow from investing is negative, it suggests that a company is reinvesting profits and expanding its operations. Conversely, positive cash flow from investing may indicate financial stress or the sale of non-core assets to refocus on core business activities.

Financing activities

This section refers to cash received from or paid to investors and creditors. Like the two previous sections, it is divided into cash inflows and cash outflows.

- Cash inflows include issuing shares or borrowing loans.

- Cash outflows include repaying loans, paying dividends, or buying back shares.

Based on the example, there is a notes payable entry in the cash flow from financing, amounting to USD 10,000. Notes payable is a borrowing agreement between a company and another party, in which the company takes out a loan and promises to repay it on a specific future date. When a loan is received, it increases the company’s total cash, resulting in a positive cash flow from financing.

A positive net cash flow from financing (CFF) indicates that a company may be issuing debt (loans or shares) to fund business expansion. Conversely, a negative CFF suggests that the company is paying off loans or returning profits to shareholders, often a sign of financial stability.

We provide CIPS practice questions with answers and detailed explanation, besides they are updated regularly to reflect the actual exam. If you want to consolidate your knowledge before the exam, you can check the links below. The discount code is HAPPYAUG25.

L4M1: https://www.udemy.com/course/cips-l4m1-practice-test-short-learning-guide/?couponCode=HAPPYAUG25

L4M2: https://www.udemy.com/course/cips-diploma-l4m2-practice-test/?couponCode=HAPPYAUG25

L4M5: https://www.udemy.com/course/cips-practice-test-commercial-negotiation/?couponCode=HAPPYAUG25

L4M7: https://www.udemy.com/course/level-4-diploma-whole-life-asset-management-l4m7/?couponCode=HAPPYAUG25

L4M8: https://www.udemy.com/course/cips-l4m8-practice-in-procurement-and-supply/?couponCode=HAPPYAUG25

L5M2: https://www.udemy.com/course/cips-l5m2-daniel-do/?couponCode=HAPPYAUG25

L5M3: https://www.udemy.com/course/l5m3-daniel/?couponCode=HAPPYAUG25

L5M4: https://www.udemy.com/course/l5m4-advanced-contract-and-finance/?couponCode=HAPPYAUG25

L5M5: https://www.udemy.com/course/l5m5-daniel/?couponCode=HAPPYAUG25