How can the balance sheet benefit the buyer during supplier appraisal? (Part 2)

In the previous post, I shared insights about the income statement and its implications for buyers. However, they may miss out some key information if they only look at the income statement. Financial statement typically includes the income statement, the balance sheet and the cashflow statement. Each offer different aspects, allowing buyers to outline a broad picture of a supplier’s financial health. The buyer needs to take them into account when assessing suppliers. In this post, I continue to analyze the balance sheet and how it helps buyers identify the potential supply risks.

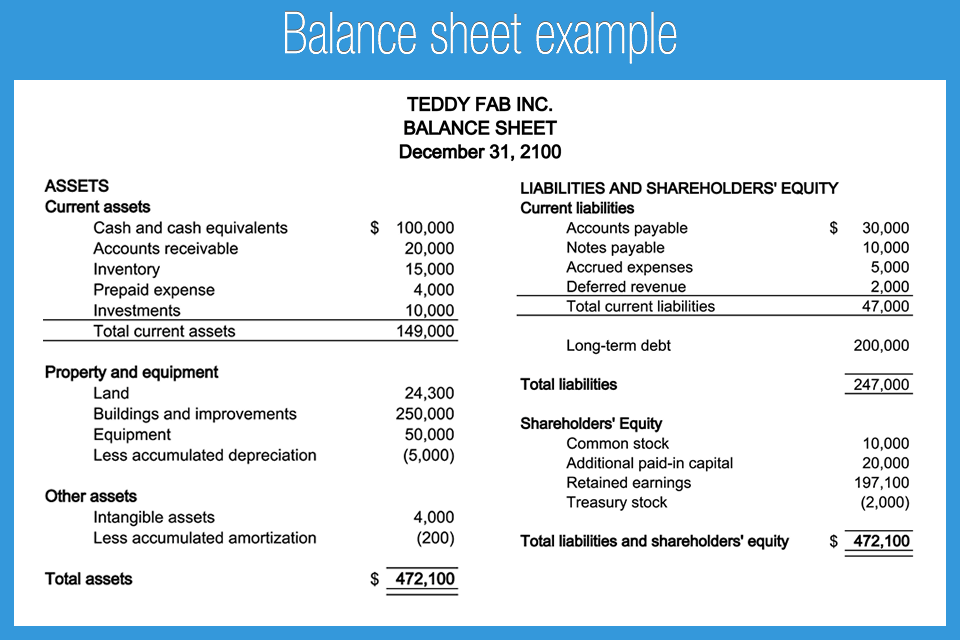

As you can see in an example of the balance sheet mentioned in the picture above. it is structured into 2 sides, based on the fundamental principle:

Total assets = Total liabilities + shareholder’s equity

The left side presents a company’s total assets while the right side shows its total liabilities and shareholder’s equity. I will introduce the basic content of each section before exploring its significance for purchasing in more depth.

Section 1: Current assets & non-current assets

This section refers to a company’s total assets used to support its operation. Current assets are those which can be easily converted into cash, or used up within one year, or within a company’s operating cycle. Non-current assets involve long-term assets such as land, building, factory and intangible assets like patents, licenses, secret formulas…

In the example:

- The total current assets are 149,000 million USD

- The long-term assets (property and equipment) = land +building & improvements + equipment – accumulated depreciation = 319,300 million USD. The word “depreciation” refers to the reduction in the value of tangible assets during their useful life. The accumulated depreciation is the total amount of depreciation expenses that has been recorded for an asset since it was accquired and put into use. When accounting for accumulated depreciation on the balance sheet, it helps reflect the true carrying value of assets on the balance sheet.

- The intangible assets = intangible assets – accumulated amortization = 3,800 million USD. The word amortization has a similar meaning to depreciation, but it is used to describe the reduction in value of intangible assets. Accumulated amortization refers to the total amount of amortization expenses that has been recorded over time. It helps determine the net book value of intangible assets.

Section 2: Current liabilities and long-term debt

In the section, the buyer can identify a supplier’s financial obligations in the short-term and long-term. Current liabilities refers to debts that are due within 1 year or within a company’s operating cycle. Long-term debt refers to financial obligations that a company is required to pay over a period longer than 1 year. Accroding the example above, the current liabilities amount to 47,000 million USD, while the long-term debt totals 200,000 million USD.

Section 3: Shareholder’s equity

This section normally includes:

- The fund that a company raises by issuing shares to the investors in exchange for shareholder stake

- Retained earning refers tothe portion of a company’s profit which is reinvested in the business.

In the example above, the fund raised through stock amount to USD 10,000 million, the addional pay-in capital is an amount of money that investors pay to a company above the par value of its stocks, which is USD 20,000 million. The retained earnings total USD 197,100 million. Treasury stock refers to shares that a company has issued and repurchased from the shareholders or in the open market, which reduce the total shareholder’s equity. That’s why the treasury stock is put in parenthesis (2000 million USD).

When looking at 3 sections, these numbers carry less meaningful insights for buyers. They need to calculate and result in financial indicators to support their purchasing decisions. Buyers are encouraged to use some useful financial indicators below:

- Liquidity Ratio: It refers to a company’s ability to fulfill its financial obligations in a short time frame. It often includes current ratio and quick ratio that I analysed in the previous post here https://en.evocurement.edu.vn/are-the-cips-exam-questions-on-current-ratio-and-quick-ratio-difficult-to-answer/. Acting as a buyer, you should choose a supplier with ratios which are greater than 1. Because this indicates their ability to maintain operations smoothly.

- Leverage Ratio: It is calculated by comparing debt to equity, reflecting how much a company finances its operation through debt and its own fund. If the supplier has a high D/E ratio, revealing that they heavily rely on debt, which may pose risks if their cash flow is unstable. Conversely, a supplier is considered more stable if they have a low D/E ratio. However, debt is not inherently bad, a low D/E ratio may limit a company’s growth.

- Efficiency Ratio & Rate of Returns: To calculate these ratios, the buyer needs to consult information from both the income statement and the balance sheet.

Asset turnover ratio is one of efficiency ratios, which is calculated by dividing the revenue by the average total assets. This ratio tells the buyer how efficiently a company manages and turns its assets into revenue. The high ratio indicates the more efficient use of assets and vice versa.

The other ratios, which the buyer should not omit, are return on equity, return on assets and return on invested capital. Each ratio carries different insights for the buyers.

Return on equity = Net Income / Shareholder’s Equity. It tells a company’s ability to generate profit based on the shareholder’s equity.

Return on assets = Net Income / Average Total Assets. Based on a buyer’s perspective, it suggests how efficiently the supplier uses its assets to generate net income.

Return on invested capital = Net Operating After Tax / Net Debt + Equity. It tells the buyer how efficiently the supplier use its debt and equity to generate profit.

The buyers are free to use different ratios and are not limited to those mentioned above. Depending on their purposes, they will calculate the appropriate ratios to support supplier appraisal and risk management.

Up to this point, the buyer may know the role of the balance sheet in evaluating suppliers, enabling them to choose a supplier with a strong financial position.

We provide CIPS practice questions with answers and detailed explanation, besides they are updated regularly to reflect the actual exam. If you want to consolidate your knowledge before the exam, you can check the links below. The discount code is HAPPYAUG25.

L4M1: https://www.udemy.com/course/cips-l4m1-practice-test-short-learning-guide/?couponCode=HAPPYAUG25

L4M2: https://www.udemy.com/course/cips-diploma-l4m2-practice-test/?couponCode=HAPPYAUG25

L4M5: https://www.udemy.com/course/cips-practice-test-commercial-negotiation/?couponCode=HAPPYAUG25

L4M7: https://www.udemy.com/course/level-4-diploma-whole-life-asset-management-l4m7/?couponCode=HAPPYAUG25

L4M8: https://www.udemy.com/course/cips-l4m8-practice-in-procurement-and-supply/?couponCode=HAPPYAUG25

L5M2: https://www.udemy.com/course/cips-l5m2-daniel-do/?couponCode=HAPPYAUG25

L5M3: https://www.udemy.com/course/l5m3-daniel/?couponCode=HAPPYAUG25

L5M4: https://www.udemy.com/course/l5m4-advanced-contract-and-finance/?couponCode=HAPPYAUG25

L5M5: https://www.udemy.com/course/l5m5-daniel/?couponCode=HAPPYAUG25